Arbitrage (Edge-Based) Example

Arbitrage exploits price differences across markets for risk-free profit. This edge-based formulation finds profitable currency cycles in a directed graph of exchange rates, where edge weights represent conversion rates between currencies.

import getpass

import os

import numpy as np

from dotenv import load_dotenv

from luna_quantum.algorithms import SCIP

from luna_usecases.arbitrage_edge_based import (

ArbitrageEdgeBasedCollection,

ArbitrageEdgeBasedData,

ArbitrageEdgeBasedFormulation,

ArbitrageEdgeBasedInstance,

)

load_dotenv()

if "LUNA_API_KEY" not in os.environ:

os.environ["LUNA_API_KEY"] = getpass.getpass("Enter your Luna API key: ")

Create Data

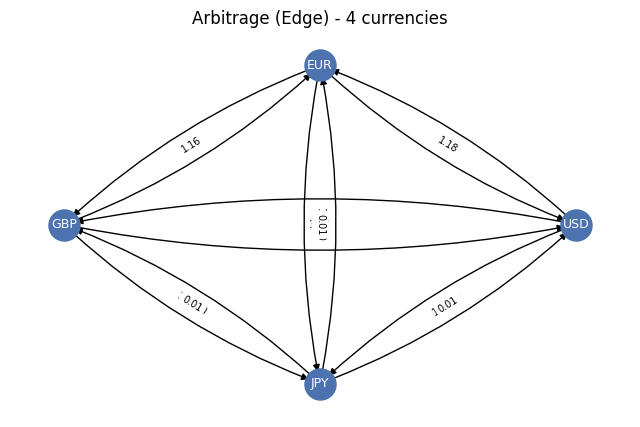

Define exchange rates between 4 currencies (USD, EUR, GBP, JPY) as a directed rate matrix.

adj = np.array(

[

[0.0, 0.85, 0.73, 110.0],

[1.18, 0.0, 0.86, 129.5],

[1.37, 1.16, 0.0, 150.7],

[0.0091, 0.0077, 0.0066, 0.0],

]

)

node_names = ["USD", "EUR", "GBP", "JPY"]

data = ArbitrageEdgeBasedData.from_adjacency_matrix(adjacency_matrix=adj, node_names=node_names)

print(data.to_string())

Arbitrage Edge-Based Data:

Currencies: USD, EUR, GBP, JPY

Number of currencies: 4

Number of directed edges: 12

Plot Data

Visualize the currency exchange rate network.

Create Formulation

Find profitable arbitrage cycles where the product of exchange rates exceeds 1.

Arbitrage Edge-Based Formulation:

Currencies: 4

Directed edges: 12

Decision Variables:

y[i,j] in {0,1} for each directed edge (i,j)

y[i,j] = 1 if edge (i,j) is in the cycle

Total: 12 binary variables

Objective:

maximize sum_(Undefined, Undefined) log(rate[i,j]) * y[i,j]

Constraints:

1. Flow conservation (4 constraints):

sum_j y[v,j] == sum_j y[j,v] for all nodes v

2. At most one outgoing edge (4 constraints):

sum_j y[v,j] <= 1 for all nodes v

3. Non-trivial cycle (1 constraint):

sum_{(i,j)} y[i,j] >= 1

Create Instance

Combine data and formulation into a solvable instance.

instance = ArbitrageEdgeBasedInstance(data=data, formulation=formulation)

print(instance.to_string())

Data:Arbitrage Edge-Based Data:

Currencies: USD, EUR, GBP, JPY

Number of currencies: 4

Number of directed edges: 12

Formulation:Arbitrage Edge-Based Formulation:

Currencies: 4

Directed edges: 12

Decision Variables:

y[i,j] in {0,1} for each directed edge (i,j)

y[i,j] = 1 if edge (i,j) is in the cycle

Total: 12 binary variables

Objective:

maximize sum_(Undefined, Undefined) log(rate[i,j]) * y[i,j]

Constraints:

1. Flow conservation (4 constraints):

sum_j y[v,j] == sum_j y[j,v] for all nodes v

2. At most one outgoing edge (4 constraints):

sum_j y[v,j] <= 1 for all nodes v

3. Non-trivial cycle (1 constraint):

sum_{(i,j)} y[i,j] >= 1

Formulate Model

Translate the instance into a mathematical optimization model.

Solve and Interpret

Solve the model with SCIP and interpret the raw result into a use-case-specific solution.

scip = SCIP()

job = scip.run(model)

sol = job.result()

uc_solution = instance.interpret(sol)

print(uc_solution.to_string())

/Users/maximilianjanetschek/PycharmProjects/luna-usecases/.venv/lib/python3.13/site-packages/rich/live.py:260:

UserWarning: install "ipywidgets" for Jupyter support

warnings.warn('install "ipywidgets" for Jupyter support')

2026-06-16 21:16:44 INFO Sleeping for 5.0 seconds. Waiting and checking a function in a loop.

2026-06-16 21:16:51 INFO Sleeping for 10.0 seconds. Waiting and checking a function in a loop.

2026-06-16 21:17:06 INFO Sleeping for 15.0 seconds. Waiting and checking a function in a loop.

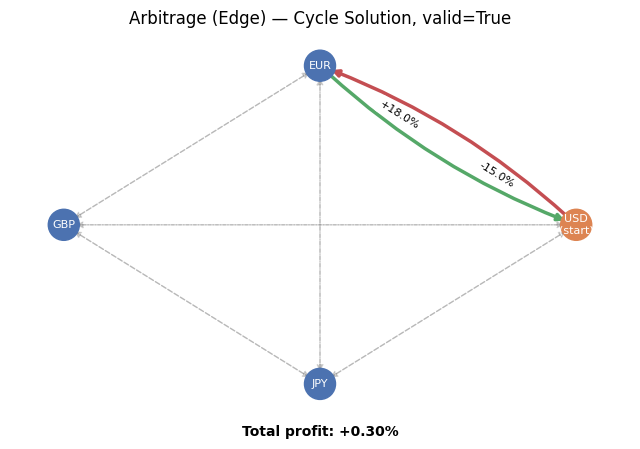

Arbitrage Edge-Based Solution:

Status: VALID

Cycle: USD->EUR -> EUR->USD

Arbitrage Profit: 1.003000

Profitable: YES

Plot Solution

Visualize the optimal solution.

Collections

Generate a benchmark collection of random instances for batch processing.

collection = ArbitrageEdgeBasedCollection.from_random(min_currencies=3, max_currencies=6, num_instances=1, seed=42)

model = collection.instances[0].formulate()

print(model)

Model: arbitrage_edge_based<s42_n3_i0>

Maximize

0.4054651081081644 * y_0_1 - 0.110616318142052 * y_0_2

- 0.1724140384186996 * y_1_0 - 0.10536051565782628 * y_1_2

- 0.10536051565782628 * y_2_0 - 0.19757889468462903 * y_2_1

Subject To

flow_conservation_0: y_0_1 + y_0_2 - y_1_0 - y_2_0 == 0

flow_conservation_1: -y_0_1 + y_1_0 + y_1_2 - y_2_1 == 0

flow_conservation_2: -y_0_2 - y_1_2 + y_2_0 + y_2_1 == 0

max_one_outgoing_0: y_0_1 + y_0_2 <= 1

max_one_outgoing_1: y_1_0 + y_1_2 <= 1

max_one_outgoing_2: y_2_0 + y_2_1 <= 1

non_trivial: y_0_1 + y_0_2 + y_1_0 + y_1_2 + y_2_0 + y_2_1 >= 1

Binary

y_0_1 y_0_2 y_1_0 y_1_2 y_2_0 y_2_1