Portfolio Optimization Problem (POP) Example

This notebook demonstrates how to use the Portfolio Optimization use case to select (without weight allocation) an optimal portfolio of assets that balances risk and return.

Overview

The Portfolio Optimization problem aims to select a subset of assets from a larger set to maximize expected returns while minimizing risk (variance). This implementation uses:

- Mean-Variance Optimization: Based on Markowitz portfolio theory

- Risk Aversion Parameter: Controls the trade-off between risk and return

- Constraint: Select exactly N assets from the available set

from datetime import datetime, timedelta

import pytz

import yfinance as yf

from dotenv import load_dotenv

from luna_quantum.algorithms import SCIP

from luna_usecases.portfolio_optimization import (

PopData,

PopFormulation,

PopInstance,

PopStockCollection,

)

Option 1: Create Data from Real Market Data (Yahoo Finance)

Use yfinance to download real historical stock returns.

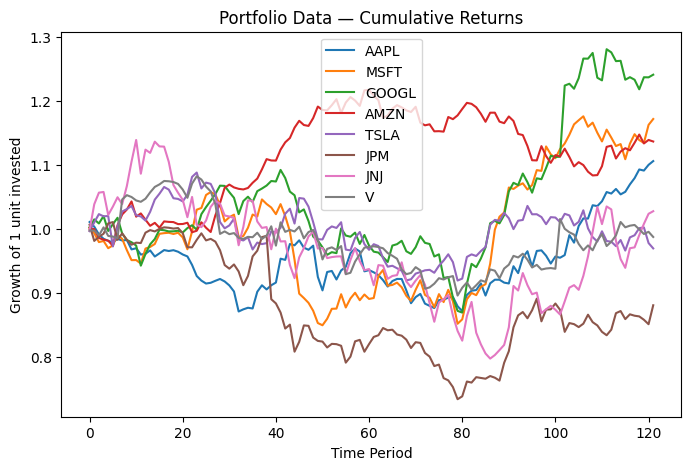

# Define portfolio of assets (stock tickers)

tickers = ["AAPL", "MSFT", "GOOGL", "AMZN", "TSLA", "JPM", "JNJ", "V"]

# Download historical data (last 6 months of daily data)

end_date = datetime.now(tz=pytz.timezone("Europe/London"))

start_date = end_date - timedelta(days=180)

data = yf.download(tickers, start=start_date, end=end_date, progress=False)

close = data["Close"]

# Calculate daily returns

daily_returns = close.pct_change().dropna()

# Convert to numpy array (assets as rows, time periods as columns)

returns_array = daily_returns.T.values

Create Portfolio Optimization Data

Create the optimization data from the downloaded returns.

data = PopData.from_returns(

returns=returns_array,

asset_names=tickers,

pick_n=3, # Select 3 assets from the 8 available

risk_aversion=1.5, # Moderate risk aversion

)

print(data.to_string())

Portfolio Optimization Data:

Number of assets: 8

Time periods: 120

Assets to select: 3

Risk aversion: 1.5

Notes:

- Returns are per period (e.g. daily returns)

- Expected return and risk are derived from this data

<Axes: title={'center': 'Portfolio Data — Cumulative Returns'}, xlabel='Time Period', ylabel='Growth of 1 unit invested'>

Create Formulation and Instance

Define the optimization formulation and create an instance.

formulation = PopFormulation()

print(formulation.to_string(data))

instance = PopInstance(data=data, formulation=formulation)

print(instance.to_string())

Portfolio Optimization Formulation:

Number of assets: 8

Assets to select (pick_n): 3

Risk aversion (lambda): 1.5

Statistical Inputs:

mu[i]: expected return of asset i (average historical return)

sigma[i,j]: covariance between asset i and j

- measures how asset returns move together

- includes both variance (risk) and correlation effects

Decision Variables:

x[i] in {0,1} for i = 0, ..., 7

x[i] = 1 if asset i is selected, 0 otherwise

Total: 8 binary variables

Objective:

minimize:

lambda * sum_{i,j} sigma_{ij} x_i x_j (portfolio risk)

- sum_i mu_i x_i (expected return)

Constraints:

1. Select exactly 3 assets:

sum_i x[i] == 3

Interpretation:

- Selected assets are equally weighted in the final portfolio

- The model trades off return vs. risk via the risk_aversion parameter

Data:Portfolio Optimization Data:

Number of assets: 8

Time periods: 120

Assets to select: 3

Risk aversion: 1.5

Notes:

- Returns are per period (e.g. daily returns)

- Expected return and risk are derived from this data

Formulation:Portfolio Optimization Formulation:

Number of assets: 8

Assets to select (pick_n): 3

Risk aversion (lambda): 1.5

Statistical Inputs:

mu[i]: expected return of asset i (average historical return)

sigma[i,j]: covariance between asset i and j

- measures how asset returns move together

- includes both variance (risk) and correlation effects

Decision Variables:

x[i] in {0,1} for i = 0, ..., 7

x[i] = 1 if asset i is selected, 0 otherwise

Total: 8 binary variables

Objective:

minimize:

lambda * sum_{i,j} sigma_{ij} x_i x_j (portfolio risk)

- sum_i mu_i x_i (expected return)

Constraints:

1. Select exactly 3 assets:

sum_i x[i] == 3

Interpretation:

- Selected assets are equally weighted in the final portfolio

- The model trades off return vs. risk via the risk_aversion parameter

Option 2: Use Pre-defined Test Instances

Alternatively, use the built-in test instances from the collection.

# Create a small test instance

test_po = PopStockCollection.create_custom_portfolio(min_n_assets=5, max_n_assets=10, pick_n=3, risk_aversion=1.5)

Model: portfolio_optimization<portfolio_optimization>

Minimize

0.00004839853014730444 * x_0 * x_1 + 0.00021837786378176122 * x_0 * x_2

+ 0.00004953810754168793 * x_0 * x_3 + 0.000028264801254607608 * x_0 * x_4

+ 0.0002824735742070878 * x_1 * x_2 + 0.00017091730885172295 * x_1 * x_3

+ 0.00014050808104901615 * x_1 * x_4 + 0.0006584727718210958 * x_2 * x_3

- 0.0006563965619213331 * x_2 * x_4 - 0.00007653454413666587 * x_3 * x_4

- 0.0011960431488212471 * x_0 - 0.00007364645664972782 * x_1

- 0.0033643644666493918 * x_2 - 0.00035540509483889633 * x_3

+ 0.004447807654524379 * x_4

Subject To

select_exactly_pick_n: x_0 + x_1 + x_2 + x_3 + x_4 == 3

Binary

x_0 x_1 x_2 x_3 x_4

Model: portfolio_optimization<portfolio_optimization>

Minimize

-0.00014291285177124268 * x_0 * x_1 + 0.000563676866500389 * x_0 * x_2

- 0.000012101750258144041 * x_0 * x_3 + 0.00017933128562777232 * x_0 * x_4

- 0.00015354357656758427 * x_0 * x_5 - 0.000029513374434255652 * x_1 * x_2

- 0.00005147970189117845 * x_1 * x_3 - 0.00026337637439990177 * x_1 * x_4

- 0.00006833410982963855 * x_1 * x_5 - 0.00011117753574754218 * x_2 * x_3

+ 0.00012932681009709588 * x_2 * x_4 - 0.0001745008703560667 * x_2 * x_5

- 0.000041278355932871454 * x_3 * x_4 + 0.000325956358742668 * x_3 * x_5

- 0.00005261350457692917 * x_4 * x_5 + 0.00031504365122486026 * x_0

+ 0.002079399936755943 * x_1 - 0.001440275146190538 * x_2

+ 0.0007855484826321216 * x_3 - 0.00171239728729508 * x_4

+ 0.005308390787488691 * x_5

Subject To

select_exactly_pick_n: x_0 + x_1 + x_2 + x_3 + x_4 + x_5 == 3

Binary

x_0 x_1 x_2 x_3 x_4 x_5

Model: portfolio_optimization<portfolio_optimization>

Minimize

0.0006462105280661721 * x_0 * x_1 + 0.00034660930106406756 * x_0 * x_2

+ 0.0003759685045828889 * x_0 * x_3 + 0.00018150932177757187 * x_0 * x_4

+ 0.0003533952212617582 * x_0 * x_5 + 0.0004031418959592822 * x_0 * x_6

+ 0.0004031019544822866 * x_1 * x_2 + 0.0004861965061493578 * x_1 * x_3

+ 0.0003019047032230202 * x_1 * x_4 + 0.0009242197768264929 * x_1 * x_5

+ 0.00034356513608994324 * x_1 * x_6 + 0.0006285430313734698 * x_2 * x_3

+ 0.0002844114288104348 * x_2 * x_4 + 0.0007919557815240384 * x_2 * x_5

+ 0.00009742114299326164 * x_2 * x_6 + 0.00034025337669320126 * x_3 * x_4

+ 0.0014203852826931691 * x_3 * x_5 + 0.0001302968019024273 * x_3 * x_6

+ 0.0003244681552307956 * x_4 * x_5 - 0.0001148556868286614 * x_4 * x_6

- 0.000010734177511946944 * x_5 * x_6 - 0.0010183650725778504 * x_0

- 0.0006858969633008603 * x_1 + 0.0014493517087124804 * x_2

+ 0.0020769818731586264 * x_3 - 0.0005600249568388085 * x_4

- 0.006766527443573074 * x_5 - 0.0008417502499780492 * x_6

Subject To

select_exactly_pick_n: x_0 + x_1 + x_2 + x_3 + x_4 + x_5 + x_6 == 3

Binary

x_0 x_1 x_2 x_3 x_4 x_5 x_6

Model: portfolio_optimization<portfolio_optimization>

Minimize

-0.0002760571658992133 * x_0 * x_1 + 0.0002246610368241246 * x_0 * x_2

+ 0.0005073066571575017 * x_0 * x_3 + 0.00032801972619909666 * x_0 * x_4

- 0.0001701554626560012 * x_0 * x_5 + 0.0003418066533321136 * x_0 * x_6

+ 0.00031409247698898507 * x_0 * x_7 + 0.000045524595711052664 * x_1 * x_2

- 0.00010639156558070483 * x_1 * x_3 - 0.00017225498817818703 * x_1 * x_4

+ 0.00022336559546613552 * x_1 * x_5 - 0.00024243047464027253 * x_1 * x_6

- 0.00028229265501875176 * x_1 * x_7 + 0.00022752386239958882 * x_2 * x_3

+ 0.00027383856043998965 * x_2 * x_4 - 0.0003263180403878334 * x_2 * x_5

+ 0.0006301300480617835 * x_2 * x_6 + 0.0002531533020121104 * x_2 * x_7

+ 0.000012933566987719995 * x_3 * x_4 - 0.00003669940234366571 * x_3 * x_5

+ 0.0004852799144554529 * x_3 * x_6 + 0.00014783184919598695 * x_3 * x_7

- 0.00033364074298019653 * x_4 * x_5 + 0.0004861965061493578 * x_4 * x_6

+ 0.00043164331012153425 * x_4 * x_7 - 0.0006168831153506087 * x_5 * x_6

- 0.00043759338568553387 * x_5 * x_7 + 0.0005326675967544576 * x_6 * x_7

+ 0.0010624317743319223 * x_0 + 0.0008763527407403841 * x_1

+ 0.0005886002126255077 * x_2 + 0.0008726722114606023 * x_3

+ 0.0020769818731586264 * x_4 - 0.001223802842801291 * x_5

- 0.0006858969633008603 * x_6 - 0.0013698664375681455 * x_7

Subject To

select_exactly_pick_n: x_0 + x_1 + x_2 + x_3 + x_4 + x_5 + x_6 + x_7 == 3

Binary

x_0 x_1 x_2 x_3 x_4 x_5 x_6 x_7

Model: portfolio_optimization<portfolio_optimization>

Minimize

-0.0003427123617863133 * x_0 * x_1 + 0.0005117504498657739 * x_0 * x_2

- 0.00016656994751006285 * x_0 * x_3 - 0.00013673709769301712 * x_0 * x_4

+ 0.00017449694672593176 * x_0 * x_5 + 0.0002395009518484987 * x_0 * x_6

+ 0.0003674230518964695 * x_0 * x_7 + 0.00034510831682350667 * x_0 * x_8

- 0.0003305749289972772 * x_1 * x_2 + 0.000170047132927894 * x_1 * x_3

+ 0.0002103631148322157 * x_1 * x_4 + 0.0004257311480005284 * x_1 * x_5

+ 0.000005737988092487298 * x_1 * x_6 - 0.00026313394531239594 * x_1 * x_7

- 0.00027672074813889073 * x_1 * x_8 - 0.000029513374434255652 * x_2 * x_3

- 0.00014291302237797842 * x_2 * x_4 + 0.00044325053784544864 * x_2 * x_5

- 0.00005147970189117845 * x_2 * x_6 + 0.0008413493683833196 * x_2 * x_7

+ 0.0005955705800052795 * x_2 * x_8 + 0.0005636769395096077 * x_3 * x_4

- 0.000036477353013386755 * x_3 * x_5 - 0.00011117753574754218 * x_3 * x_6

- 0.00030153879873133147 * x_3 * x_7 - 0.00024625092473421937 * x_3 * x_8

- 0.00003522599224060468 * x_4 * x_5 - 0.00001210181950025394 * x_4 * x_6

- 0.0002364621295267268 * x_4 * x_7 - 0.0002435767806282072 * x_4 * x_8

+ 0.00001861491129915443 * x_5 * x_6 + 0.0002011432884315894 * x_5 * x_7

+ 0.0003814459340939113 * x_5 * x_8 + 0.000015053736192647862 * x_6 * x_7

+ 0.00028210424148152307 * x_6 * x_8 + 0.000713564231815507 * x_7 * x_8

- 0.00007364645664972782 * x_0 - 0.0017069190515922397 * x_1

+ 0.002079399936755943 * x_2 - 0.001440275146190538 * x_3

+ 0.0003150442917945556 * x_4 - 0.0027941036297724547 * x_5

+ 0.0007855484826321216 * x_6 - 0.0008085119947233421 * x_7

- 0.001427619539525738 * x_8

Subject To

select_exactly_pick_n: x_0 + x_1 + x_2 + x_3 + x_4 + x_5 + x_6 + x_7 + x_8 ==

3

Binary

x_0 x_1 x_2 x_3 x_4 x_5 x_6 x_7 x_8

Model: portfolio_optimization<portfolio_optimization>

Minimize

0.0002960892420491974 * x_0 * x_1 + 0.000726584320505193 * x_0 * x_2

+ 0.00024493203009092336 * x_0 * x_3 + 0.0003994765646518248 * x_0 * x_4

+ 0.0003677524268749083 * x_0 * x_5 - 0.0002039608661092726 * x_0 * x_6

+ 0.00021593382252928266 * x_0 * x_7 + 0.00021527440032983281 * x_0 * x_8

+ 0.0005126684299053083 * x_0 * x_9 + 0.0003038759195784823 * x_1 * x_2

+ 0.00015915293908873112 * x_1 * x_3 + 0.00037742071805781937 * x_1 * x_4

+ 0.0000546127474415468 * x_1 * x_5 - 0.00016665809100937175 * x_1 * x_6

+ 0.0002041775299243057 * x_1 * x_7 + 0.0002506121609271246 * x_1 * x_8

+ 0.0001510998094192494 * x_1 * x_9 + 0.00016386566718014058 * x_2 * x_3

+ 0.0006012081966530213 * x_2 * x_4 + 0.00031203117117038634 * x_2 * x_5

- 0.00024357678726457294 * x_2 * x_6 + 0.00033747604109070784 * x_2 * x_7

+ 0.00028703161319412903 * x_2 * x_8 + 0.0007540008425274127 * x_2 * x_9

+ 0.00023488100752084383 * x_3 * x_4 + 0.0002193242089413195 * x_3 * x_5

+ 0.000008846291023625101 * x_3 * x_6 - 0.00023001955321648427 * x_3 * x_7

+ 0.000035496556896427736 * x_3 * x_8 + 0.00007252920210969622 * x_3 * x_9

+ 0.00043195202456718996 * x_4 * x_5 - 0.00017825542887839476 * x_4 * x_6

+ 0.00026608421200469097 * x_4 * x_7 + 0.00023082264813676056 * x_4 * x_8

+ 0.00037655315352002456 * x_4 * x_9 + 0.00000801425235041558 * x_5 * x_6

+ 0.00006276202196567495 * x_5 * x_7 + 0.00008389296292310444 * x_5 * x_8

+ 0.00024717900311282194 * x_5 * x_9 - 0.000023009912806236203 * x_6 * x_7

+ 0.000046737099146110155 * x_6 * x_8 - 0.00004218232898763118 * x_6 * x_9

+ 0.00014068922708810336 * x_7 * x_8 + 0.00023420859357452923 * x_7 * x_9

+ 0.00022274834123899733 * x_8 * x_9 + 0.0014644999294661377 * x_0

- 0.0011005247517895686 * x_1 - 0.0014276196714528215 * x_2

- 0.001196042215390995 * x_3 + 0.0019131705118662038 * x_4

+ 0.0014113827804667042 * x_5 + 0.00031504365122486026 * x_6

- 0.00035105225661627415 * x_7 + 0.000797699785225212 * x_8

+ 0.0009712156051786558 * x_9

Subject To

select_exactly_pick_n: x_0 + x_1 + x_2 + x_3 + x_4 + x_5 + x_6 + x_7 + x_8

+ x_9 == 3

Binary

x_0 x_1 x_2 x_3 x_4 x_5 x_6 x_7 x_8 x_9

Formulate and Solve

Create the quantum optimization model and solve it.

# Formulate the model

model = instance.formulate()

load_dotenv()

solver = SCIP()

job = solver.run(model)

solution = job.result()

uc_solution = instance.interpret(solution)

/Users/maximilianjanetschek/PycharmProjects/luna-usecases/.venv/lib/python3.13/site-packages/rich/live.py:260:

UserWarning: install "ipywidgets" for Jupyter support

warnings.warn('install "ipywidgets" for Jupyter support')

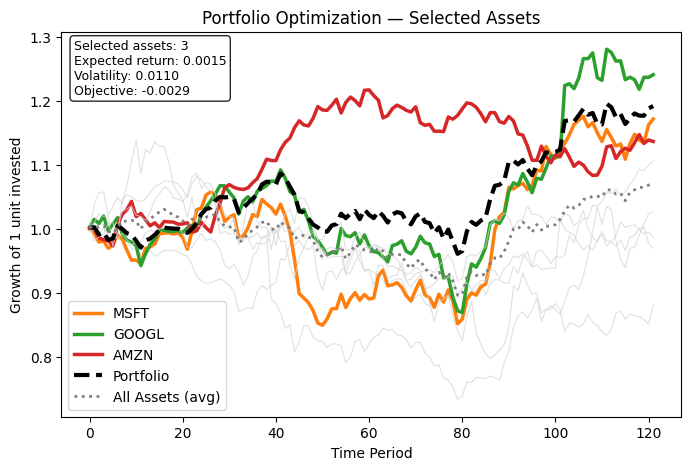

Portfolio Optimization Solution:

Status: VALID

Selected Assets (3): AAPL, GOOGL, AMZN

Performance (per period):

Expected Return: 0.001225

Variance (Risk): 0.000100

Volatility (Std): 0.010019

Return/Risk Ratio: 0.122234

Optimization:

Objective Value: -0.002319

(lower is better; combines risk and return via risk_aversion)

<Axes: title={'center': 'Portfolio Optimization — Selected Assets'}, xlabel='Time Period', ylabel='Growth of 1 unit invested'>