Dynamic Portfolio Optimization Example

Portfolio optimization selects assets to balance return and risk. This dynamic variant extends classical Markowitz theory across multiple time periods and incorporates transaction costs when rebalancing portfolios.

In this formulation, asset selections are optimized jointly over all time steps. The model assumes that expected returns and risk estimates are known for each period, resulting in a globally optimal sequence of portfolio decisions.

This corresponds to an offline optimization setting (also referred to as perfect foresight), where future information is available during optimization. As such, the model provides a theoretical benchmark for multi-period portfolio allocation rather than a directly implementable trading strategy.

import getpass

import os

from datetime import datetime, timedelta

import pytz

import yfinance as yf

from dotenv import load_dotenv

from luna_quantum.algorithms import SCIP

from luna_usecases.dynamic_portfolio_optimization import (

DynamicPoCollection,

DynamicPoData,

DynamicPoFormulation,

DynamicPoInstance,

)

load_dotenv()

if "LUNA_API_KEY" not in os.environ:

os.environ["LUNA_API_KEY"] = getpass.getpass("Enter your Luna API key: ")

Download Historical Market Data

We start by selecting a set of assets and downloading historical price data.

From these prices, we compute daily returns, which will serve as the basis for estimating: - expected returns - risk (covariance)

tickers = ["AAPL", "MSFT", "GOOGL", "AMZN", "TSLA", "JPM", "JNJ", "V"]

end_date = datetime.now(tz=pytz.timezone("Europe/London"))

start_date = end_date - timedelta(days=180)

stock_data = yf.download(tickers, start=start_date, end=end_date, progress=False)

close = stock_data["Close"]

daily_returns = close.pct_change().dropna()

returns = daily_returns.values # shape: (T, N)

From Static Returns to Time-Dependent Estimates

In a static portfolio model, we would compute a single: - expected return vector μ - covariance matrix Σ

However, in a dynamic setting, these quantities change over time.

To model this, we estimate:

- μ[t]: expected returns at time step t

- Σ[t]: covariance matrix at time step t

using a rolling window over past observations.

Rolling Window Estimation

We use a rolling window of fixed size to estimate statistics from recent data.

For each time step t:

- we look at the last window observations

- compute the average return (μ[t])

- compute the covariance matrix (Σ[t])

This means that each estimate is based only on past observations relative to t.

However, note that in the subsequent optimization step, all time steps are considered jointly.

As a result, while the statistical estimates themselves do not use future data, the overall optimization still operates in an offline setting with access to all time steps simultaneously.

window = 10 # rolling window

data = DynamicPoData.from_returns(

tickers=tickers,

returns=returns,

window=window,

pick_n=3,

risk_aversion=1.5,

transaction_cost=0.01,

)

data = DynamicPoData(

tickers=["AAPL", "GOOGL", "MSFT"],

expected_returns=[[0.05, 0.08, 0.03], [0.06, 0.04, 0.07]],

covariance_matrices=[

np.array([[0.04, 0.01, 0.005], [0.01, 0.09, 0.02], [0.005, 0.02, 0.03]]),

np.array([[0.05, 0.015, 0.01], [0.015, 0.07, 0.025], [0.01, 0.025, 0.04]]),

],

n_assets=3,

n_time_steps=2,

pick_n=2,

risk_aversion=1.0,

transaction_cost=0.01,

)

print(data.to_string())

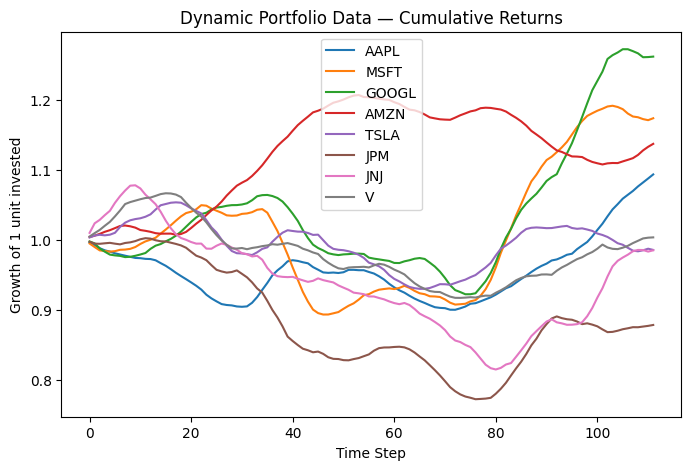

Plot Data

Visualize expected returns and risk across time periods.

<Axes: title={'center': 'Dynamic Portfolio Data — Cumulative Returns'}, xlabel='Time Step', ylabel='Growth of 1 unit invested'>

Create Formulation

Optimize multi-period asset allocation balancing returns, risk, and transaction costs.

Dynamic Portfolio Optimization Formulation:

Assets: 8

Time steps: 110

Pick per period: 3

Risk aversion: 1.5

Transaction cost: 0.01

Decision Variables:

x[t,i] in {0,1} for t = 0, ..., 109, i = 0, ..., 7

x[t,i] = 1 if asset i is selected at time step t

z[t,i] in {0,1} for t = 1, ..., 109, i = 0, ..., 7

z[t,i] = 1 if asset i changes between t-1 and t

Total: 1752 binary variables

Objective:

maximize sum_t sum_i mu[t][i]*x[t,i]

- risk_aversion * sum_t sum_{{i,j}} sigma[t][i][j]*x[t,i]*x[t,j]

- transaction_cost * sum_{{t>0}} sum_i z[t,i]

Constraints:

1. Pick exactly 3 assets per period (110 constraints):

sum_i x[t,i] == 3 for all t = 0, ..., 109

2. Transaction cost linearization (1744 constraints):

z[t,i] >= x[t,i] - x[t-1,i] for all t = 1, ..., 109, i = 0, ..., 7

z[t,i] >= x[t-1,i] - x[t,i] for all t = 1, ..., 109, i = 0, ..., 7

Create Instance

Combine data and formulation into a solvable instance.

Data:Dynamic Portfolio Optimization Data:

Tickers: AAPL, MSFT, GOOGL, AMZN, TSLA, JPM, JNJ, V

Number of assets: 8

Time steps: 110

Assets to select per period: 3

Risk aversion: 1.5

Transaction cost: 0.01

Formulation:Dynamic Portfolio Optimization Formulation:

Assets: 8

Time steps: 110

Pick per period: 3

Risk aversion: 1.5

Transaction cost: 0.01

Decision Variables:

x[t,i] in {0,1} for t = 0, ..., 109, i = 0, ..., 7

x[t,i] = 1 if asset i is selected at time step t

z[t,i] in {0,1} for t = 1, ..., 109, i = 0, ..., 7

z[t,i] = 1 if asset i changes between t-1 and t

Total: 1752 binary variables

Objective:

maximize sum_t sum_i mu[t][i]*x[t,i]

- risk_aversion * sum_t sum_{{i,j}} sigma[t][i][j]*x[t,i]*x[t,j]

- transaction_cost * sum_{{t>0}} sum_i z[t,i]

Constraints:

1. Pick exactly 3 assets per period (110 constraints):

sum_i x[t,i] == 3 for all t = 0, ..., 109

2. Transaction cost linearization (1744 constraints):

z[t,i] >= x[t,i] - x[t-1,i] for all t = 1, ..., 109, i = 0, ..., 7

z[t,i] >= x[t-1,i] - x[t,i] for all t = 1, ..., 109, i = 0, ..., 7

Formulate Model

Translate the instance into a mathematical optimization model.

Solve and Interpret

Solve the model with SCIP and interpret the raw result into a use-case-specific solution.

scip = SCIP()

job = scip.run(model)

sol = job.result()

uc_solution = instance.interpret(sol)

print(uc_solution.to_string())

/Users/maximilianjanetschek/PycharmProjects/luna-usecases/.venv/lib/python3.13/site-packages/rich/live.py:260:

UserWarning: install "ipywidgets" for Jupyter support

warnings.warn('install "ipywidgets" for Jupyter support')

2026-06-16 21:16:44 INFO Sleeping for 5.0 seconds. Waiting and checking a function in a loop.

2026-06-16 21:16:51 INFO Sleeping for 10.0 seconds. Waiting and checking a function in a loop.

2026-06-16 21:17:04 INFO Sleeping for 15.0 seconds. Waiting and checking a function in a loop.

Dynamic Portfolio Optimization Solution:

Status: VALID

Period 0: MSFT, GOOGL, AMZN

Period 1: MSFT, GOOGL, AMZN

Period 2: MSFT, GOOGL, AMZN

Period 3: MSFT, GOOGL, AMZN

Period 4: MSFT, GOOGL, AMZN

Period 5: MSFT, GOOGL, AMZN

Period 6: MSFT, GOOGL, AMZN

Period 7: MSFT, GOOGL, AMZN

Period 8: MSFT, GOOGL, AMZN

Period 9: MSFT, GOOGL, AMZN

Period 10: MSFT, GOOGL, AMZN

Period 11: MSFT, GOOGL, AMZN

Period 12: MSFT, GOOGL, AMZN

Period 13: MSFT, GOOGL, AMZN

Period 14: MSFT, GOOGL, AMZN

Period 15: MSFT, GOOGL, AMZN

Period 16: MSFT, GOOGL, AMZN

Period 17: MSFT, GOOGL, AMZN

Period 18: MSFT, GOOGL, AMZN

Period 19: AAPL, GOOGL, AMZN

Period 20: AAPL, GOOGL, AMZN

Period 21: AAPL, AMZN, TSLA

Period 22: AAPL, AMZN, TSLA

Period 23: AAPL, AMZN, TSLA

Period 24: AAPL, AMZN, TSLA

Period 25: AAPL, AMZN, TSLA

Period 26: AAPL, AMZN, TSLA

Period 27: AAPL, AMZN, TSLA

Period 28: AAPL, AMZN, TSLA

Period 29: AAPL, AMZN, TSLA

Period 30: AAPL, AMZN, TSLA

Period 31: AAPL, AMZN, TSLA

Period 32: AAPL, AMZN, TSLA

Period 33: AAPL, MSFT, AMZN

Period 34: AAPL, MSFT, AMZN

Period 35: AAPL, MSFT, AMZN

Period 36: AAPL, MSFT, AMZN

Period 37: AAPL, MSFT, AMZN

Period 38: AAPL, MSFT, AMZN

Period 39: MSFT, AMZN, JPM

Period 40: MSFT, AMZN, JPM

Period 41: MSFT, AMZN, JPM

Period 42: MSFT, AMZN, JPM

Period 43: MSFT, AMZN, JPM

Period 44: MSFT, AMZN, JPM

Period 45: MSFT, AMZN, JPM

Period 46: MSFT, AMZN, JPM

Period 47: MSFT, AMZN, JPM

Period 48: MSFT, AMZN, JPM

Period 49: MSFT, AMZN, JPM

Period 50: MSFT, AMZN, JPM

Period 51: MSFT, AMZN, TSLA

Period 52: MSFT, AMZN, TSLA

Period 53: MSFT, AMZN, TSLA

Period 54: MSFT, AMZN, TSLA

Period 55: MSFT, AMZN, TSLA

Period 56: MSFT, AMZN, TSLA

Period 57: MSFT, AMZN, TSLA

Period 58: MSFT, AMZN, TSLA

Period 59: MSFT, AMZN, TSLA

Period 60: MSFT, AMZN, TSLA

Period 61: MSFT, AMZN, TSLA

Period 62: MSFT, AMZN, TSLA

Period 63: MSFT, AMZN, TSLA

Period 64: MSFT, GOOGL, TSLA

Period 65: MSFT, GOOGL, TSLA

Period 66: MSFT, GOOGL, TSLA

Period 67: MSFT, GOOGL, TSLA

Period 68: MSFT, GOOGL, TSLA

Period 69: MSFT, GOOGL, JPM

Period 70: MSFT, GOOGL, JPM

Period 71: MSFT, GOOGL, JPM

Period 72: MSFT, GOOGL, JPM

Period 73: MSFT, GOOGL, JPM

Period 74: MSFT, GOOGL, JPM

Period 75: MSFT, GOOGL, JPM

Period 76: MSFT, GOOGL, JPM

Period 77: MSFT, GOOGL, JPM

Period 78: MSFT, GOOGL, JPM

Period 79: MSFT, GOOGL, JPM

Period 80: AAPL, MSFT, GOOGL

Period 81: AAPL, MSFT, GOOGL

Period 82: AAPL, MSFT, GOOGL

Period 83: AAPL, MSFT, GOOGL

Period 84: AAPL, MSFT, GOOGL

Period 85: AAPL, GOOGL, JNJ

Period 86: AAPL, GOOGL, JNJ

Period 87: AAPL, GOOGL, JNJ

Period 88: AAPL, GOOGL, JNJ

Period 89: AAPL, GOOGL, JNJ

Period 90: AAPL, GOOGL, JNJ

Period 91: AAPL, JPM, JNJ

Period 92: AAPL, JPM, JNJ

Period 93: AAPL, JPM, JNJ

Period 94: AAPL, JPM, JNJ

Period 95: AAPL, AMZN, JPM

Period 96: AAPL, AMZN, JPM

Period 97: AAPL, AMZN, JPM

Period 98: AAPL, AMZN, JPM

Period 99: AAPL, AMZN, JPM

Period 100: AAPL, AMZN, JPM

Period 101: AAPL, AMZN, JPM

Period 102: AAPL, AMZN, JPM

Period 103: AAPL, AMZN, JPM

Period 104: AAPL, AMZN, JPM

Period 105: AMZN, TSLA, JPM

Period 106: AMZN, TSLA, JPM

Period 107: AMZN, TSLA, JPM

Period 108: AMZN, TSLA, JPM

Period 109: AMZN, TSLA, JPM

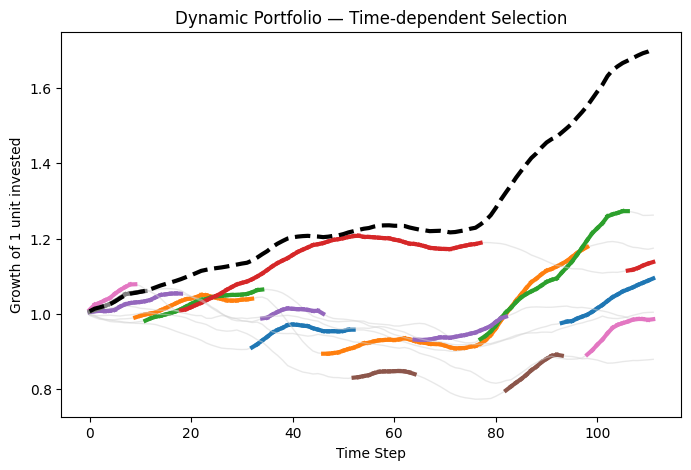

Portfolio Return: 1.456639

Portfolio Risk: 0.115417

Transaction Costs: 0.240000

Plot Solution

Visualize the optimal solution.

<Axes: title={'center': 'Dynamic Portfolio — Time-dependent Selection'}, xlabel='Time Step', ylabel='Growth of 1 unit invested'>

Collections

Generate a benchmark collection of random instances for batch processing.

collection = DynamicPoCollection.from_random(

min_assets=3, max_assets=6, n_time_steps=2, pick_n=2, num_instances=1, seed=42

)

model = collection.instances[0].formulate()

print(model)

Model: dynamic_portfolio_optimization<s42_n3_i0>

Maximize

-0.00031845908234652613 * x_0_0 * x_0_1 - 0.005378824097872742 * x_0_0 * x_0_2

- 0.003801733038977486 * x_0_1 * x_0_2 + 0.006563805484193941 * x_1_0 * x_1_1

- 0.006438512615851617 * x_1_0 * x_1_2 - 0.006590377259410821 * x_1_1 * x_1_2

+ 0.03303333549964048 * x_0_0 + 0.013952958333736984 * x_0_1

+ 0.052749880094328724 * x_0_2 + 0.03631039904708676 * x_1_0

+ 0.021702789925954542 * x_1_1 + 0.04562590629288803 * x_1_2 - 0.01 * z_1_0

- 0.01 * z_1_1 - 0.01 * z_1_2

Subject To

pick_n_period_0: x_0_0 + x_0_1 + x_0_2 == 2

pick_n_period_1: x_1_0 + x_1_1 + x_1_2 == 2

tc_pos_1_0: x_0_0 - x_1_0 + z_1_0 >= 0

tc_neg_1_0: -x_0_0 + x_1_0 + z_1_0 >= 0

tc_pos_1_1: x_0_1 - x_1_1 + z_1_1 >= 0

tc_neg_1_1: -x_0_1 + x_1_1 + z_1_1 >= 0

tc_pos_1_2: x_0_2 - x_1_2 + z_1_2 >= 0

tc_neg_1_2: -x_0_2 + x_1_2 + z_1_2 >= 0

Binary

x_0_0 x_0_1 x_0_2 x_1_0 x_1_1 x_1_2 z_1_0 z_1_1 z_1_2