Portfolio Optimization with Investment Bands Example

Portfolio Optimization with investment bands extends the classical Markowitz mean-variance framework by introducing lower and upper bounds on the allocation of each asset.

The goal is to construct a portfolio that balances expected return and risk while respecting asset-specific investment constraints. The model is formulated as a quadratic optimization problem and discretised using binary variables to make it compatible with QUBO-based solvers.

Objective

The model optimizes the classical mean-variance trade-off:

- maximize expected portfolio return

- penalize portfolio variance according to a risk aversion parameter λ

Decision Variables

Each asset allocation is represented through binary variables that discretise the continuous investment range within predefined bounds:

- binary variables encode discrete allocation levels per asset

- continuous investments are reconstructed from these binary encodings

Constraints

- Each asset must lie within its investment band \([lower_i, upper_i]\)

- The total portfolio investment must not exceed a given budget

Model Assumptions

- Expected returns are known and deterministic

- Covariance matrix is given and static

- No transaction costs or market impact are considered

- Asset returns are modeled using a mean-variance approximation

- Discretisation is introduced solely for compatibility with QUBO solvers and does not represent a financial assumption

Interpretation

The resulting solution defines a discretised portfolio allocation, which approximates a continuous mean-variance optimal portfolio within the imposed constraints.

import getpass

import os

import numpy as np

from dotenv import load_dotenv

from luna_quantum.algorithms import SCIP

from luna_usecases.portfolio_optimization_with_investment_bands import (

PoIbtvCollection,

PoIbtvData,

PoIbtvFormulation,

PoIbtvInstance,

)

load_dotenv()

if "LUNA_API_KEY" not in os.environ:

os.environ["LUNA_API_KEY"] = getpass.getpass("Enter your Luna API key: ")

Create Data

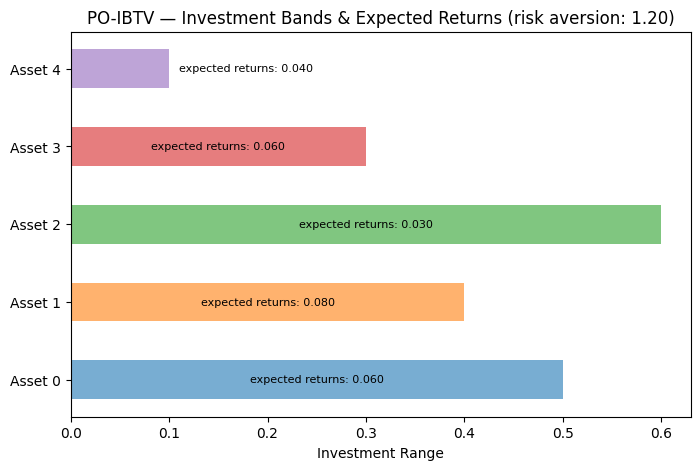

Define 3 assets with log returns, covariance matrix, and investment band constraints.

data = PoIbtvData.from_values(

log_returns=[0.06, 0.08, 0.03, 0.06, 0.04],

covariance_matrix=np.array(

[

[0.04, 0.01, 0.005, 0.008, 0.006],

[0.01, 0.09, 0.02, 0.015, 0.01],

[0.005, 0.02, 0.03, 0.01, 0.007],

[0.008, 0.015, 0.01, 0.05, 0.012],

[0.006, 0.01, 0.007, 0.012, 0.04],

]

),

investment_bands=[

(0.0, 0.5),

(0.0, 0.4),

(0.0, 0.6),

(0.0, 0.3),

(0.0, 0.1),

],

risk_aversion=1.2,

max_budget=1.0,

n_bits=3,

)

print(data.to_string())

Portfolio Optimization with Investment Bands Data:

Number of assets: 5

Discretization bits: 3

Risk aversion: 1.2

Max budget: 1.0

Assets:

Asset 0: return=0.0600, band=[0.0000, 0.5000]

Asset 1: return=0.0800, band=[0.0000, 0.4000]

Asset 2: return=0.0300, band=[0.0000, 0.6000]

Asset 3: return=0.0600, band=[0.0000, 0.3000]

Asset 4: return=0.0400, band=[0.0000, 0.1000]

Plot Data

Visualize asset returns and investment band constraints.

<Axes: title={'center': 'PO-IBTV — Investment Bands & Expected Returns (risk aversion: 1.20)'}, xlabel='Investment Range'>

Create Formulation

Allocate assets within investment bands while constraining portfolio volatility.

PO Investment Bands Formulation:

Assets: 5

Bits per asset: 3

Risk aversion: 1.2000

Max budget: 1.0

Decision Variables:

x[i,q] in {0,1} for i = 0, ..., 4, q = 0, ..., 2

x[i,q] encodes the binary decomposition of asset i allocation

Total: 15 binary variables

Objective:

maximize sum_i return[i] * investment[i]

- risk_aversion * sum_(Undefined, Undefined) sigma[i,j] * investment[i] * investment[j]

Constraints:

1. Budget constraint (1 constraint):

sum_i investment[i] <= 1.0

Create Instance

Combine data and formulation into a solvable instance.

Data:Portfolio Optimization with Investment Bands Data:

Number of assets: 5

Discretization bits: 3

Risk aversion: 1.2

Max budget: 1.0

Assets:

Asset 0: return=0.0600, band=[0.0000, 0.5000]

Asset 1: return=0.0800, band=[0.0000, 0.4000]

Asset 2: return=0.0300, band=[0.0000, 0.6000]

Asset 3: return=0.0600, band=[0.0000, 0.3000]

Asset 4: return=0.0400, band=[0.0000, 0.1000]

Formulation:PO Investment Bands Formulation:

Assets: 5

Bits per asset: 3

Risk aversion: 1.2000

Max budget: 1.0

Decision Variables:

x[i,q] in {0,1} for i = 0, ..., 4, q = 0, ..., 2

x[i,q] encodes the binary decomposition of asset i allocation

Total: 15 binary variables

Objective:

maximize sum_i return[i] * investment[i]

- risk_aversion * sum_(Undefined, Undefined) sigma[i,j] * investment[i] * investment[j]

Constraints:

1. Budget constraint (1 constraint):

sum_i investment[i] <= 1.0

Formulate Model

Translate the instance into a mathematical optimization model.

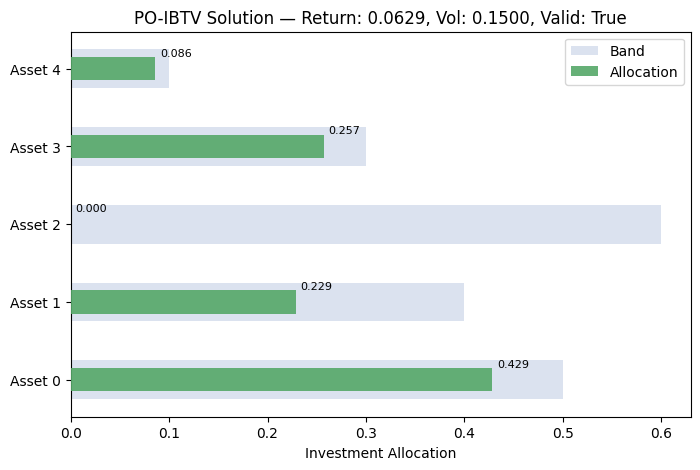

Solve and Interpret

Solve the model with SCIP and interpret the raw result into a use-case-specific solution.

scip = SCIP()

job = scip.run(model)

sol = job.result()

uc_solution = instance.interpret(sol)

print(uc_solution.to_string())

/Users/maximilianjanetschek/PycharmProjects/luna-usecases/.venv/lib/python3.13/site-packages/rich/live.py:260:

UserWarning: install "ipywidgets" for Jupyter support

warnings.warn('install "ipywidgets" for Jupyter support')

2026-06-16 21:18:12 INFO Sleeping for 5.0 seconds. Waiting and checking a function in a loop.

Portfolio Optimization with Investment Bands Solution:

Status: VALID

Asset 0: 0.428571

Asset 1: 0.228571

Asset 2: 0.000000

Asset 3: 0.257143

Asset 4: 0.085714

Portfolio Return: 0.062857

Portfolio Volatility: 0.149988

Plot Solution

Visualize the optimal solution.

<Axes: title={'center': 'PO-IBTV Solution — Return: 0.0629, Vol: 0.1500, Valid: True'}, xlabel='Investment Allocation'>

Collections

Generate a benchmark collection of random instances for batch processing.

collection = PoIbtvCollection.from_random(min_assets=2, max_assets=5, n_bits=3, num_instances=1, seed=42)

model = collection.instances[0].formulate()

print(model)

Model: portfolio_optimization_with_investment_bands<s42_n2_i0>

Maximize

-0.0000009342133667775807 * x_0_0 * x_0_1

- 0.0000018684267335551613 * x_0_0 * x_0_2

- 0.0000020134260094036983 * x_0_0 * x_1_0

- 0.000004026852018807397 * x_0_0 * x_1_1

- 0.000008053704037614793 * x_0_0 * x_1_2

- 0.0000037368534671103227 * x_0_1 * x_0_2

- 0.000004026852018807397 * x_0_1 * x_1_0

- 0.000008053704037614793 * x_0_1 * x_1_1

- 0.000016107408075229586 * x_0_1 * x_1_2

- 0.000008053704037614793 * x_0_2 * x_1_0

- 0.000016107408075229586 * x_0_2 * x_1_1

- 0.00003221481615045917 * x_0_2 * x_1_2

- 0.0000625820943834702 * x_1_0 * x_1_1

- 0.0001251641887669404 * x_1_0 * x_1_2

- 0.0002503283775338808 * x_1_1 * x_1_2 + 0.003015164703338624 * x_0_0

+ 0.00602986229999386 * x_0_1 + 0.012057856173254165 * x_0_2

+ 0.0010399817128410014 * x_1_0 + 0.002048672378490268 * x_1_1

+ 0.003972180568213595 * x_1_2

Subject To

budget: 0.0681327191380834 * x_0_0 + 0.1362654382761668 * x_0_1

+ 0.2725308765523336 * x_0_2 + 0.06097222791097653 * x_1_0

+ 0.12194445582195305 * x_1_1 + 0.2438889116439061 * x_1_2 <=

0.9385909856669729

Binary

x_0_0 x_0_1 x_0_2 x_1_0 x_1_1 x_1_2